Where are Foreclosures in 2015?

The housing debacle of the last decade had a very wide swath and affected borrowers, banks and investors--not just here in the United States but abroad, too. Massive waves of foreclosures hit the market and very few areas were left untouched. But there were and still are two waves of foreclosures and they occur in judicial and non-judicial states.

Why Care about this?

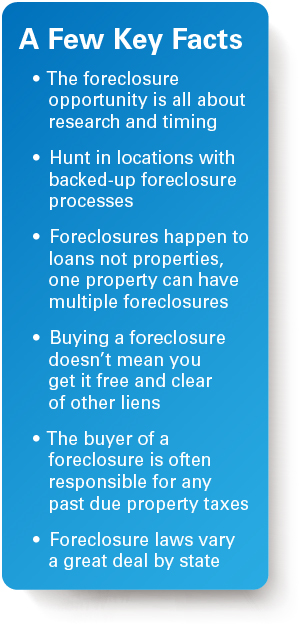

The main reason to understand the difference between the two processes and waves is that most of the foreclosures after the meltdown in non-judicial states have been sold. It’s that simple, there just isn’t the same opportunity to pick up run down assets. This doesn’t mean there aren’t great opportunities to make money in non-judicial states; it’s just that the opportunity to buy foreclosures is significantly bigger in judicial states right now.

There are still amazing deals

in judicial

foreclosure states

The foreclosure process varies by state, and depends on whether the state uses the court system to file a foreclosure. The judicial foreclosure process requires court action on a foreclosed home and can take a very long time. The real estate crisis created a big opportunity to buy distressed properties and there are still amazing deals in judicial foreclosure states.

Judical and

Non-Judical States

So How Does This Work? |

The Judicial Foreclosure

Judicial foreclosure occurs when the lender files a civil lawsuit against the borrower and the court handles it all. It starts when the lender files their lawsuit, at which time they also file a lis pendens (LIS) on the property. The LIS is a document recorded with the County Recorder’s office, to let possible buyers, lenders, and others know of the pending foreclosure lawsuit.

HINT: here is your first signal of a pre-foreclosure.

A second notice, the Notice of Foreclosure Sale (NFS), is normally filed once the court has set the auction timing.

These judicial foreclosures can be split into two basic types: foreclosure by sale, and strict foreclosure.

- Foreclosure by sale requires the home to be auctioned to the highest bidder with the lender placing the first, or opening, bid. These auctions are often called sheriff sales.

- In a strict foreclosure, the court sets a date by which the owner must pay the mortgage, and if the owner doesn’t pay, then the court gives ownership of the home to the lender.

Non-Judicial Foreclosure

The non-judicial foreclosure process allows a lender to advertise and sell the property at a public auction, without going through the court system. They still need to follow the rules defined by their state and is sometimes called a “Statutory Foreclosure” for this reason. The process starts when the lender files a Notice of Default (NOD) with the County Recorder’s office, putting the homeowner and anyone else who is interested on notice that the loan may be foreclosed on. A second notice, the Notice of Trustee Sale is typically filed 30 to 120 days later, depending on the state; and sets the auction date and time. In a few states, only the Notice of Trustee Sale is recorded.

The key difference for non-judicial foreclosures is that the borrower agreed to the process when they took the loan based on some language agreed to in the documentation. Usually a Power of Sale clause is added to the mortgage or deed of trust that gives a third-party trustee the right to sell the property in the event the borrower defaults. This avoids the need for a court’s involvement and allows the lender to follow a state-defined process and it moves a lot quicker.

Foreclosure Tips

Know Before You Go

Let’s step aside from foreclosures for a second and imagine you’re going to make an offer on an existing home pulled from the Multiple Listing Service. You go to an open house and you make an offer. But before you do, you get to review the Seller’s Property Disclosure. Sellers are required to list any known issues regarding the property that may affect its value. If the basement was flooded last spring, that event should be noted. If the hot water heater doesn’t heat very well, it will be listed. If there are items discovered after a sale that were not disclosed but should have been, sellers can be held liable for the repairs and in some states sued for damages.

A foreclosed property, however, may not have such a disclosure list. In fact, if the home is going up for sale at an auction it’s likely you’ll never be able to walk through the property until after the home is yours. You can only look through a window or take a peek in the back yard. This is the danger zone. Don’t buy a property without having it thoroughly inspected by a licensed property inspector. Borrowers who go for an extended period not being able to afford the house payments also won’t have the money to keep up the property. Buying a foreclosure without an inspection can cost you later on down the line.

Using a Buyer’s Agent

You can scour the Internet on your own for foreclosed properties but your best move is to locate a real estate agent who can find foreclosures for you. Banks that foreclose on homes keep them in their inventory and usually hire local real estate agents to list the homes. Such properties will typically have had any needed repairs completed and if not the issues will be listed on the Seller’s Disclosure.

Using an experienced agent to find your next investment can help not just by finding properties quicker but also by crafting a strategic offer. If you’re going to flip the property you’ll need to make enough to pay the associated closing costs when selling, and if you’re going to keep it and rent it out your agent can research market rents for the area as well.

SUMMARY

- The foreclosure opportunity is still alive today

- You probably want to search in judicial states to find the best deals

- Foreclosure laws vary a great deal by state

- Use a buyer’s agent to help find and negotiate foreclosed homes